Drive growth with an ACH payments partner

Easy sign-up. Flat rate pricing. Fast Settlement. Change the way you get paid.

Get Paid

Online, mobile, in-store and recurring ACH payments. Enjoy increased productivity and faster deposits.

Business Intelligence

A modern ACH payment gateway with all the tools you need to maximize your efficiency.

IT'S ALL IN THE NUMBERS

A true payments partner, not just an API.

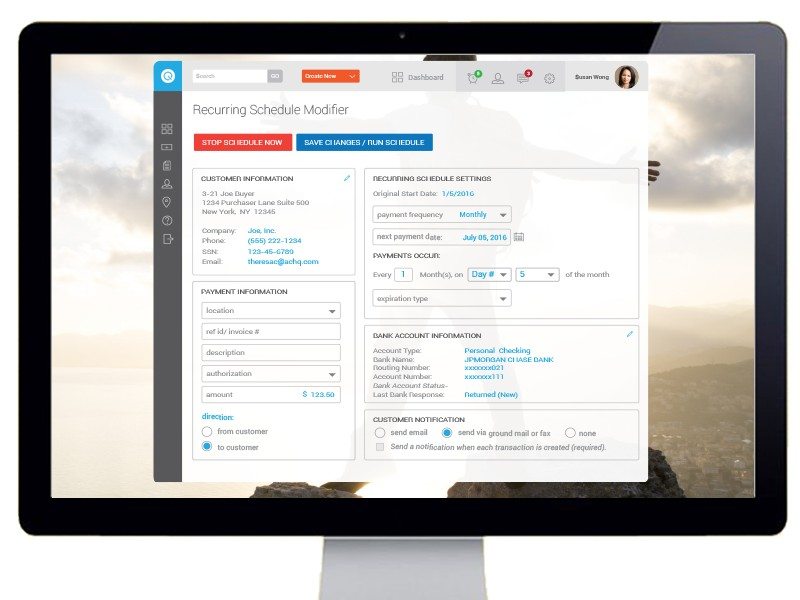

Customers can sign up to a plan or subscription to make recurring payments to your business. Save time, stop human errors and avoid failed payments.

Keep up-to-date on the status of all your payments with our online dashboard and multi-channel notifications.

We have long-term servicing and technical relationships with some of the largest and

most well established companies in the world.

You’ll be in great company.

OUR CORE SERVICES

ACH

Use our cloud-based payment gateway to accept ACH payments from clients’ accounts for a fast and secure ACH processing solution.

eCheck Processing

You control your settlements. Get next-day funding with this ACH alternative and grow your business.

Card Processing

Seamless and scalable credit and debit card processing solutions across all of your business channels.

Bank Account Verification

Stops fraud, identity theft, and non-sufficient fund fees before they cost you money or ruin your users’ experience.

Convenience Fee

Businesses are able to enjoy fast, and reliable, card and eCheck payment processing at no cost and no increased operating expenses.

ACHQ Portal

Full-featured and easy to integrate, our payment gateway is friendly for both merchants and developers.

Business Insights with the ACHQ Payment Portal

Portal is built for executives and teams of small to medium businesses who are frustrated by having to run

time-consuming reports with scattered information. With Portal, you get the ACH processing solution

you need, how and when you need it. A trend chart with clear revenue and sale indicators along

with a summary of sales revenue, refunds and reversals makes business analysis a breeze. Portal can process recurring ACH payments automatically, making your life a bit easier.

{kind=link}

{kind=link}

{kind=link}